Repo Rate & Inflation, Explained Simply (2026)

Repo rate (5.25%) and inflation (3.48%) explained in plain English — and how they affect your home-loan EMI and property prices in India and Tamil Nadu, with the latest 2026 figures.

What is inflation, in plain words?

Inflation is simply prices going up over time — which means the same ₹100 buys a little less each year. A cup of filter coffee that cost ₹10 a few years ago is ₹20 today. The coffee did not change; your rupee just got smaller. That shrinking is inflation.

When economists say inflation is 3.48%, they mean a typical family's basket of goods — food, fuel, rent, clothes — costs about 3.48% more than it did a year ago (India's latest actual retail CPI, for April 2026). A little inflation is normal and even healthy; the Reserve Bank of India (RBI) aims to keep it gentle and predictable, around 4%.

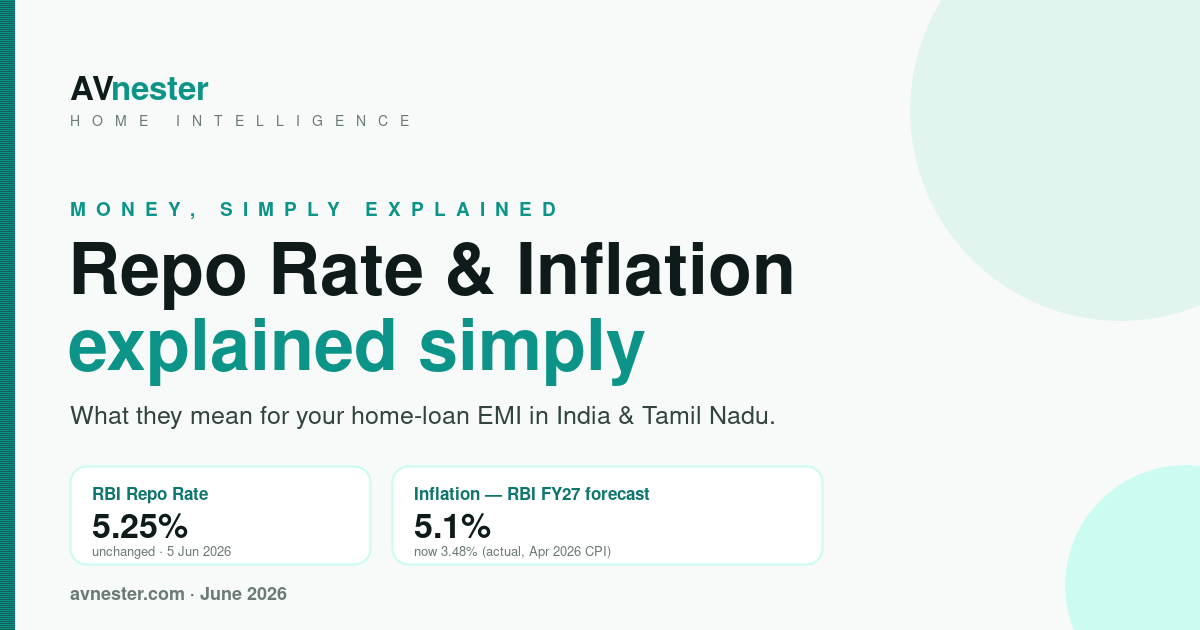

You may also see a higher figure of 5.1% quoted — that is the RBI's forecast for the full year FY2026-27 (raised from 4.6% on 5 June 2026), a projection for the year ahead, not today's rate. So both are correct: 3.48% is what inflation is now, and 5.1% is where the RBI expects it to average over the coming year.

What is the repo rate?

The repo rate is the interest the RBI charges banks when they borrow money from it for a short time. Think of it as the wholesale price of money in the country. Banks borrow from the RBI, then lend to you as home loans and car loans — so if the RBI's price goes up, your loan gets pricier; if it falls, loans get cheaper.

As of June 2026 the repo rate is 5.25%. The RBI left it unchanged on 5 June 2026 with a neutral stance, meaning it is ready to move either way depending on what inflation does next. Two related rates you may hear: the SDF (5.0%), what banks earn parking spare cash with the RBI, and the MSF (5.5%), an emergency higher rate.

How they work together (the see-saw)

The RBI uses the repo rate as a thermostat for prices, and the two move in opposite directions on purpose.

When inflation runs too high, the RBI raises the repo rate. Loans get costlier, people spend a little less, and prices settle. When inflation is low or soft, the RBI can cut the repo rate to make loans cheaper and give the economy a nudge.

Today inflation is soft (3.48%) and the repo rate is on hold (5.25%) — a calm, wait-and-watch setting. For a home buyer, calm is good: your EMI stays stable and predictable.

What it means for your home loan EMI

Most home loans today are repo-linked, so your interest rate moves with the RBI repo rate — usually within a few months of a change.

A small rate change makes a real monthly difference. On a ₹50 lakh loan over 20 years at about 8.5% (the repo rate plus a typical bank spread), the EMI is roughly ₹43,391 per month. A 0.25% rate change works out to about ₹800 per month — close to ₹1.9 lakh over the full loan.

Don't guess your number. Use the AVnester EMI Calculator at /tools/emi-calculator to see your exact monthly payment, and the Affordability Calculator at /tools/what-can-i-afford to find a comfortable budget from your income.

What it means for property prices in Tamil Nadu

Inflation does not just raise coffee — it raises cement, steel, land and labour. Over the years that pushes home prices up too, which is the quiet cost of waiting: a home you delay may simply cost more later.

A home loan is one of the few good borrowings — you lock today's price, then repay with rupees that are gently shrinking, so inflation works for you here. But budget the full cost. In Tamil Nadu, stamp duty is 7% of the property value and registration is 4%, totalling 11% — on a ₹50 lakh property in Coimbatore that is ₹3.5 lakh stamp duty plus ₹2 lakh registration, ₹5.5 lakh in all. Estimate yours with the Stamp Duty Calculator at /tools/stamp-duty-calculator.

The sweet spot is exactly today's setting: soft inflation and steady rates — predictable EMIs and prices that are not spiking. A sensible window to buy within your budget, not above it.

The smart-buyer checklist

• Know your comfortable EMI — and stress-test it for a 0.5% rate rise. • Prefer repo-linked home loans — they are transparent and fall quickly when the RBI cuts. • Improve your CIBIL score to 750+ — it can shave your rate more than RBI moves do. • Don't try to time the market perfectly — buy the right home within budget; rates average out over 20 years. • Keep an emergency buffer of about 6 months of EMIs, so a rate rise never stresses you.

Frequently asked questions

What is the repo rate in simple words? The repo rate is the interest rate at which the RBI lends money to banks for the short term — the wholesale price of money. When it rises, loans get costlier; when it falls, cheaper. As of June 2026 it is 5.25%.

What is the current repo rate and inflation in India in 2026? The RBI repo rate is 5.25% (held steady on 5 June 2026 with a neutral stance). The latest actual retail inflation (CPI) is 3.48% for April 2026, below the RBI's 4% target. Separately, the RBI's forecast for FY2026-27 is 5.1% (raised from 4.6% on 5 June 2026) — a projection for the year ahead, not the current rate.

How does the repo rate affect my home loan EMI? Most home loans are repo-linked, so your rate moves with the repo rate. On a ₹50 lakh, 20-year loan, a 0.25% change is about ₹800 per month, or roughly ₹1.9 lakh over the loan.

Is now a good time to buy a home in Tamil Nadu? With inflation soft (3.48%) and the repo rate steady (5.25%), EMIs are stable and prices are not spiking — a sensible window to buy within your budget. This is general information, not financial advice.

What is the difference between the repo rate and inflation? Inflation is how fast everyday prices rise (now 3.48%). The repo rate (now 5.25%) is the RBI's main tool to control it — raised to cool high inflation, cut when inflation is low.